Most drivers think their standard auto policy covers ignition interlock devices required for hardship licenses. It doesn't—and finding out after installation can cost you thousands in denied claims.

What Standard Auto Insurance Actually Covers on Vehicles with IIDs

Your standard auto insurance policy covers collision damage to your vehicle, liability for injuries you cause, and comprehensive losses like theft or vandalism. It does not cover damage to, theft of, or malfunction of an ignition interlock device unless you purchase a separate equipment endorsement.

Most carriers treat IIDs as aftermarket electronic equipment, similar to custom stereos or GPS units. Base policies exclude aftermarket equipment by default. If your IID is stolen, vandalized, or damaged in an accident, you will pay the replacement cost out of pocket—typically $200 to $400 for the unit itself, plus reinstallation fees that run $75 to $150.

This gap matters most during the hardship license period. You cannot legally drive without a functioning IID, and replacement delays mean lost work days. Some states require proof of IID installation before issuing the hardship license at all. If your device is damaged and your policy does not cover it, you are stuck paying cash replacement costs while the clock runs on your suspension.

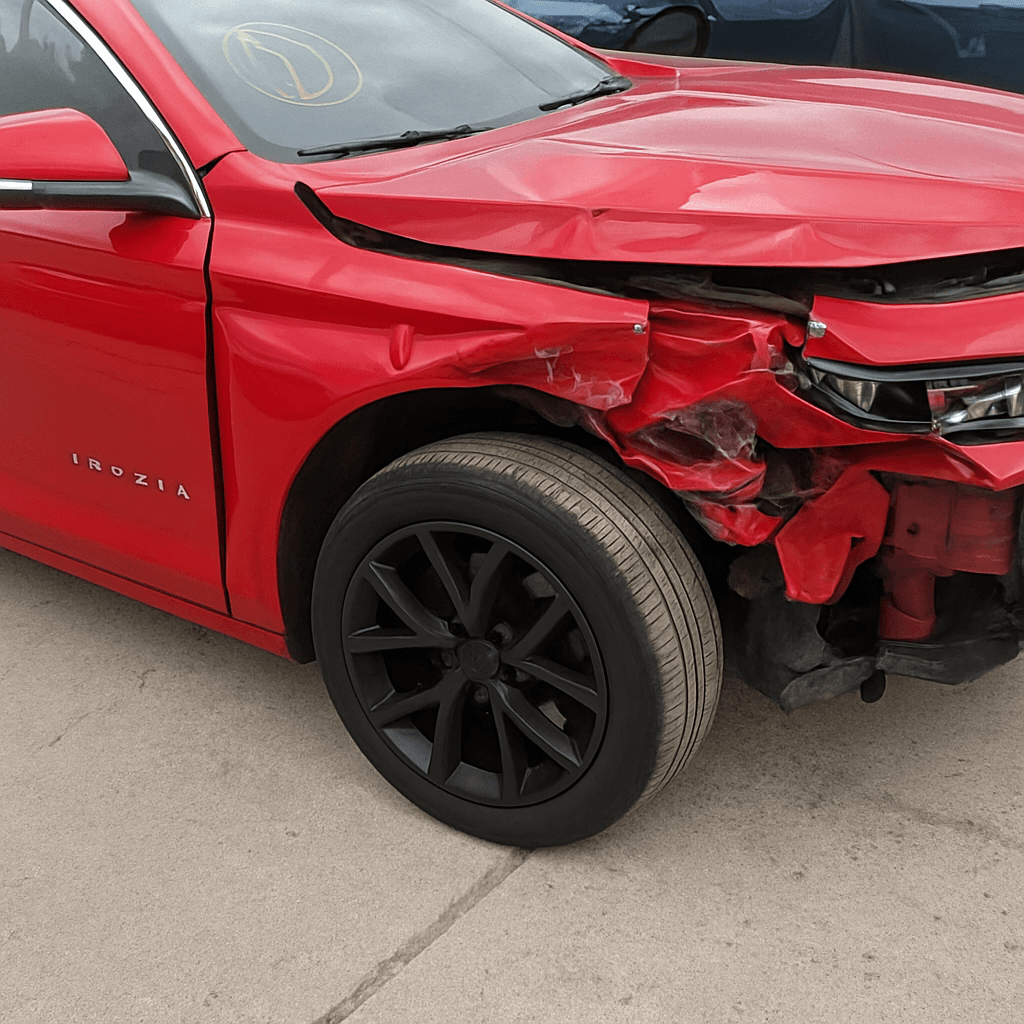

Why IID Damage Happens More Often Than Drivers Expect

Ignition interlock devices fail for predictable reasons. Cold weather causes sensor malfunctions in northern states—Montana, North Dakota, Wisconsin, and Michigan drivers report devices failing to start in subzero temperatures, triggering lockout events that look like violations to the monitoring agency.

Parking lot fender-benders damage dashboard-mounted handsets. Thieves target IID-equipped vehicles because the visible device signals a restricted driver who may not report the theft immediately. Vandalism is common in apartment complexes where neighbors recognize the device.

The device itself costs $200 to $400 to replace, but the real cost is the interruption. Most states require 24 to 72 hours advance notice to your monitoring company before disconnecting the device for any reason. If your IID is stolen or damaged and you drive without it, even to get it replaced, your hardship license is revoked. You pay for a tow, a rental, and the device replacement simultaneously.

Compare car insurance rates in your state

Get quotes from licensed carriers — no obligation, no spam, results in minutes.

Get Your Free Quote✓ No Obligation Required✓ Licensed Carriers Only✓ Available Nationwide✓ Free to Compare

Equipment Endorsements That Cover IID Replacement and Repair

Carriers offer custom equipment endorsements or electronic equipment coverage riders that extend your policy to cover aftermarket devices. Cost varies by carrier, but most charge $5 to $15 per month for $1,000 to $2,500 in equipment coverage.

This endorsement covers theft, vandalism, and accidental damage to the IID. It does not cover device malfunction due to user error—blowing into the device after eating or drinking triggers false positives, and those costs remain your responsibility. It does not cover normal wear or calibration fees, which your lease agreement with the IID provider already covers.

Not all carriers offer this endorsement to high-risk drivers. Progressive, The General, and Bristol West explicitly offer equipment coverage to SR-22 and hardship license drivers. State Farm and Allstate require underwriter approval for drivers with DUI convictions. If your current carrier refuses the endorsement, you will need to shop non-standard carriers who specialize in restricted-license coverage.

How IID Lease Agreements Interact with Insurance Coverage

Your IID provider requires a lease agreement when the device is installed. Most agreements include a damage liability clause: you are responsible for the full replacement cost if the device is stolen, vandalized, or damaged. Lease agreements typically run $75 to $125 per month and cover calibration, maintenance, and technical support—but not theft or collision damage.

If you file an insurance claim for IID damage, the payout goes to you, not the lease provider. You must use that payout to replace the device with the same provider or pay an early termination fee before switching providers. Most states require you to use a state-certified IID vendor, and not all vendors are certified in every county.

Some lease agreements include optional damage waivers for $10 to $20 per month. These waivers cover theft and vandalism but exclude collision damage. If you already carry an equipment endorsement on your auto policy, the lease damage waiver is redundant. If your carrier refuses equipment coverage, the lease waiver is your only option.

State-Specific IID Requirements That Affect Insurance Needs

States vary on who pays for IID installation, monitoring, and removal. Arizona, Oregon, and Washington require the state to cover costs for low-income drivers. Most states require the driver to pay all costs, and insurance does not reimburse those fees even with an equipment endorsement.

Some states mandate IID installation for all hardship licenses tied to DUI or refusal charges. Others require it only for repeat offenders. Florida, Virginia, and West Virginia require IIDs for all DUI-related hardship licenses, even first-time offenders. Texas, Georgia, and Oklahoma allow first-time offenders to petition for hardship without IID if the BAC was below 0.15.

If your state requires an IID and your policy does not cover it, you are legally required to drive with an uninsured device. If you are rear-ended and the impact damages the handset, you pay replacement costs even though you were not at fault. The at-fault driver's liability policy covers your vehicle damage, not aftermarket equipment you added post-purchase.

What to Do Before Installing an IID on a Hardship License

Call your insurance agent before scheduling IID installation. Ask whether your current policy covers aftermarket electronic equipment. If it does not, request a quote for a custom equipment endorsement or electronic equipment rider. If your carrier refuses, ask for a written denial—you will need it when shopping other carriers.

Get quotes from non-standard carriers who specialize in high-risk and restricted-license drivers. Compare the cost of adding equipment coverage to your current policy versus switching carriers entirely. Some non-standard carriers bundle SR-22 filing, liability coverage, and equipment coverage into a single monthly premium that costs less than adding endorsements to a standard policy.

Document your IID installation with photos and receipts. If you file a claim later, your carrier will require proof of the device's value and proof it was installed by a state-certified vendor. Keep your lease agreement and calibration records in your vehicle—law enforcement and DMV auditors will ask for them during traffic stops and hardship license reviews.